+91-9646339590

+91-9646339590

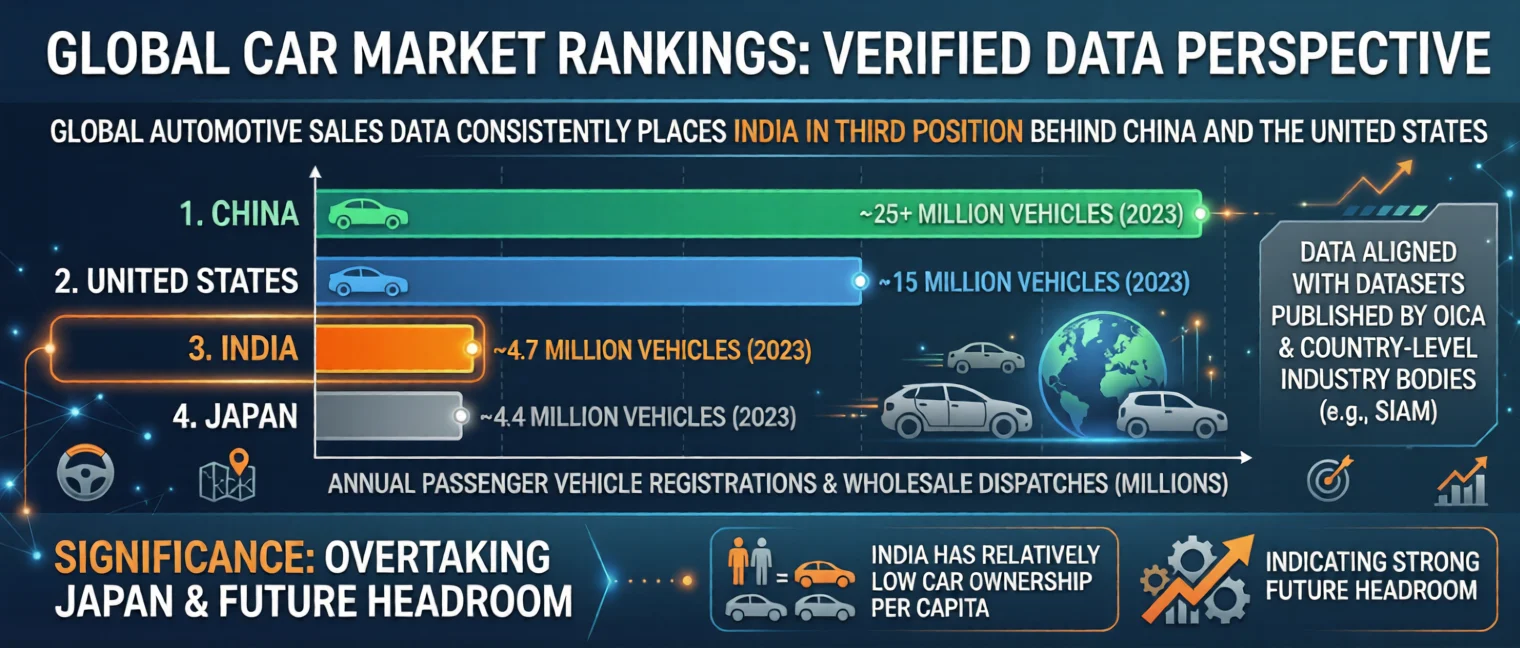

India has moved ahead of Japan to become the world’s third largest car market, a transition confirmed through sustained sales momentum between 2022 and 2024. This shift is supported by verified industry data rather than short-term fluctuations. According to the OICA global automotive database, India recorded approximately 4.7 million passenger vehicle sales in 2023, edging past Japan’s ~4.4 million units. The gap, while not massive, signals a structural change in global automotive demand.

Unlike mature markets where growth is incremental, India’s rise is being driven by first-time ownership, segment shifts toward SUVs, and a rapidly expanding manufacturing ecosystem. This combination has turned India into a volume-driven market with increasing strategic importance for global automakers.

Why did India overtake Japan in car sales?

India overtook Japan due to higher first-time car buyers, rapid SUV demand, and expanding financing access, while Japan’s market remains mature with slower growth.

Global Car Market Rankings: Verified Data Perspective

Global automotive sales data consistently places India in the third position behind China and the United States. The ranking is based on annual passenger vehicle registrations and wholesale dispatches:

1. China – ~25+ million vehicles annually (2023)

2. United States – ~15 million vehicles annually (2023)

3. India – ~4.7 million vehicles annually (2023)

4. Japan – ~4.4 million vehicles annually (2023)

These figures are aligned with datasets published by OICA and country-level industry bodies such as the Society of Indian Automobile Manufacturers (SIAM). The significance lies not just in overtaking Japan, but in India achieving this position while still having relatively low car ownership per capita, indicating strong future headroom.

Demand-Side Transformation: What Is Driving India’s Growth?

1. First-Time Buyers Dominating Market Expansion

A large portion of India’s passenger vehicle growth is coming from first-time buyers upgrading from two-wheelers. SIAM data suggests that in several high-growth regions, over 40% of new car buyers are entering the four-wheeler segment for the first time. This trend is particularly visible in Tier-2 and Tier-3 cities where financing penetration has improved significantly.

Unlike Japan, where replacement demand dominates, India’s market is still in an expansion phase driven by new ownership.

2. SUV Segment Reshaping the Market Structure

The most defining shift in India’s car market is the dominance of SUVs. As of 2024, SUVs contribute more than 50% of total passenger vehicle sales. Compact and mid-size SUVs such as Hyundai Creta (Hyundai’s compact SUV platform known for premium features and strong urban demand), Tata Nexon (India’s top-selling SUV with a 5-star Global NCAP safety rating), and Maruti Suzuki Brezza have consistently led monthly sales charts.

This shift is not purely aspirational. It is influenced by road conditions, higher seating position preference, and perceived safety benefits. Additionally, manufacturers have localized SUV production, making them price-competitive with premium hatchbacks.

During peak demand cycles in 2023–2024, waiting periods for high-demand SUVs extended to 3–5 months, indicating supply-demand imbalance and strong consumer preference.

3. Price Sensitivity and the Decline of Entry-Level Cars

While overall volumes are rising, the entry-level hatchback segment has shown contraction. Industry estimates indicate a 15–20% decline in entry-level car sales after the implementation of BS6 emission norms due to increased production costs.

This has led to a “premiumization effect,” where buyers are stretching budgets toward compact SUVs instead of entry-level cars. Automakers are adjusting product portfolios accordingly.

4. Financing Ecosystem and Digital Retail Evolution

The role of financing cannot be understated. Over 70% of car purchases in India are now financed through loans, with faster approvals driven by digital verification systems. Automakers have integrated end-to-end digital purchase journeys, allowing customers to select, finance, and book vehicles online.

This reduced friction has played a measurable role in expanding demand beyond metro cities.

5. Manufacturing Scale and Export Capability

India is not just a consumption market; it is increasingly a production hub. Companies like Maruti Suzuki and Hyundai export vehicles from India to over 100 countries. According to SIAM, India exported over 6 lakh passenger vehicles in FY2023–24.

Government-backed initiatives such as the Production-Linked Incentive (PLI) scheme have further strengthened domestic manufacturing, especially in advanced automotive technologies and EV components.

Why Japan’s Market Has Plateaued

Japan’s automotive market reflects maturity rather than decline. High vehicle ownership rates, aging population, and efficient public transport systems limit incremental demand. Additionally, urban congestion and parking constraints discourage additional car ownership in cities like Tokyo.

Another structural factor is vehicle lifecycle. Japanese consumers tend to retain vehicles longer, reducing replacement frequency. While Japan continues to lead in hybrid technology and automotive engineering, domestic volume growth remains stable.

Electrification and Hybrid Strategy: India vs Japan

India’s EV adoption is at an early but accelerating stage. According to the Society of Manufacturers of Electric Vehicles (SMEV), electric passenger vehicle sales crossed 90,000 units in 2023, with strong year-on-year growth driven by government incentives under FAME II.

At the same time, hybrid technology is gaining traction as a transitional solution. Models like the Grand Vitara and Hyryder are contributing to hybrid adoption in the mass market.

Japan, in contrast, has long been a leader in hybrid vehicles, with widespread adoption of models such as the Toyota Prius. However, this technological leadership has not translated into domestic volume expansion due to market saturation.

For deeper insights into EV trends and future projections, refer to McKinsey automotive industry research.

Regulatory Evolution and Safety Standards

India’s automotive growth is increasingly aligned with global regulatory standards. The transition to BS6 emission norms has significantly reduced vehicle emissions. Additionally, the introduction of Bharat NCAP in 2023 is pushing manufacturers to improve crash safety performance.

Mandatory safety features such as dual airbags, ABS, and reverse parking sensors have raised baseline safety levels across segments. This regulatory push is gradually improving overall vehicle quality.

Challenges That Could Influence Future Growth

1. Urban Congestion and Infrastructure Pressure

Rapid vehicle growth without proportional urban planning has led to congestion in major cities. Parking shortages and traffic density could act as limiting factors for future growth in metro regions.

2. Rising Ownership Costs

Higher vehicle prices, insurance premiums, and fuel costs are impacting affordability, particularly in the entry-level segment.

3. EV Infrastructure Gaps

Charging infrastructure remains uneven, especially outside major cities. Range anxiety and charging time continue to influence EV adoption decisions.

4. Supply Chain Volatility

Global semiconductor shortages in recent years exposed vulnerabilities in automotive supply chains, affecting production timelines and delivery schedules.

Future Outlook: Can India Move Beyond Third Position?

India’s long-term growth potential remains strong due to its demographic advantage and low car penetration rate (cars per 1,000 people). Industry forecasts suggest that India’s passenger vehicle market could cross 6 million units annually by 2030 if economic growth remains stable.

However, surpassing the United States will depend on multiple factors, including income growth, infrastructure expansion, and EV ecosystem maturity. The trajectory is positive, but not guaranteed.

Conclusion

India overtaking Japan as the world’s third largest car market is not an isolated milestone—it represents a shift in how global automotive demand is distributed. The country’s growth is rooted in structural factors such as first-time ownership, manufacturing scale, and evolving consumer preferences.

At the same time, the market faces real challenges, including rising costs and infrastructure constraints. Sustained growth will depend on how effectively these issues are addressed alongside the transition toward cleaner mobility.

Want more insights on India’s EV future and SUV trends? Explore our latest analysis on EV adoption, charging infrastructure, and upcoming electric vehicles in India.

Key Takeaways

– India surpassed Japan in passenger vehicle sales around 2022–2023

– SUV demand and first-time buyers are primary growth drivers

– Entry-level car segment is shrinking due to cost pressures

– EV adoption is growing but infrastructure remains a constraint

– India’s market still has strong long-term expansion potential

Frequently Asked Questions (FAQs)

1. When did India become the third largest car market?

India overtook Japan around 2022 based on annual passenger vehicle sales, with the position stabilizing in subsequent years.

2. What is driving India’s car market growth?

Growth is driven by first-time buyers, SUV demand, improved financing access, and expanding infrastructure.

3. Why is Japan’s car market not growing?

Japan’s market is mature, with high ownership rates, aging population, and strong public transport systems limiting demand growth.

4. Which car segment is growing the fastest in India?

The SUV segment, particularly compact SUVs, is the fastest-growing category in India.

5. Is India’s EV market significant yet?

EVs are still a small portion of total sales but are growing rapidly due to government incentives and increasing awareness.

6. Can India become the second largest car market?

It is possible in the long term, but it will depend on sustained economic growth and infrastructure development.

About the Author

Ankush Kumar is a seasoned automotive analyst with expertise in Indian and global car markets, electric vehicle technologies, and vehicle safety trends. He delivers insightful, data-driven analysis backed by authoritative sources such as SIAM, OICA, and leading global automotive research firms.

Follow him on Facebook: Ankush Kumar